Carmignac's Note

With a vibrant economy and markets, is Europe now taking revenge?

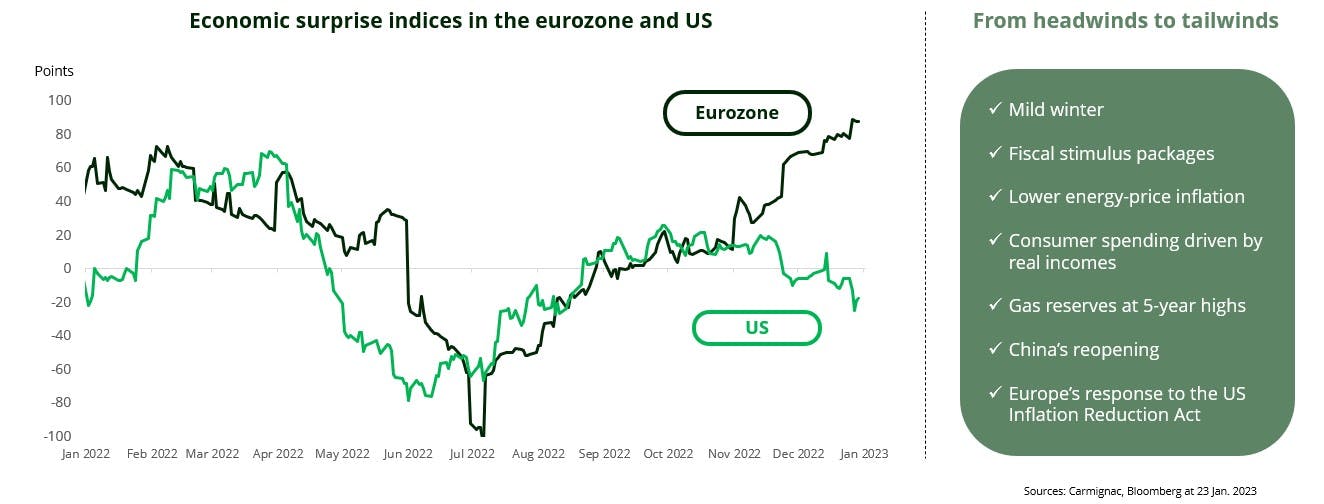

Europe’s economy has outshone that of the United States in the past few weeks, as reflected in the two regions’ economic surprise indicators.

Why is that?

A combination of factors has led Europe to outperform: a mild winter, which has improved the energy situation; fiscal stimulus packages; and the reopening of China’s economy. The upshot has been a spectacular rally in European stocks. Since 31 August 2022, they are up 17.5% more than their US counterparts, and 23.5% if you factor in the euro’s appreciation against the dollar1.

Europe’s relative strength will inevitably suffer some setbacks – this kind of outperformance has to pause for breath occasionally if it’s to last. We therefore don’t believe the stellar run in European equities will necessarily continue in the near term. However, we do believe that this trend reversal in favour of Europe, after the US led the way for most of the past 12 years, is part of a structural shift that is just now beginning.

Who will benefit from this new trend?

The renewed inflationary environment that began to take hold in the developed world in 2021 will likely encourage capital to flow from the west (i.e. the US) to the east (i.e. Europe, China, and Japan) as investors realise that the more cyclical economies stand to experience higher-than-expected growth rates. This will push up European, Chinese, and Japanese equity markets significantly, since they tend to have more cyclical stocks, and have lagged over the past decade of persistently anaemic growth.

What’s more, companies operating in sectors that have typically been more useful to the real economy should get a boost from today’s more justifiable level of interest rates.

1Based on gains in the Euro Stoxx 50 vs the S&P 500